Address

234 Lower Gilmore Rd

Campton KY 41301

Work Hours

Monday to Friday: 9AM - 5PM

Address

234 Lower Gilmore Rd

Campton KY 41301

Work Hours

Monday to Friday: 9AM - 5PM

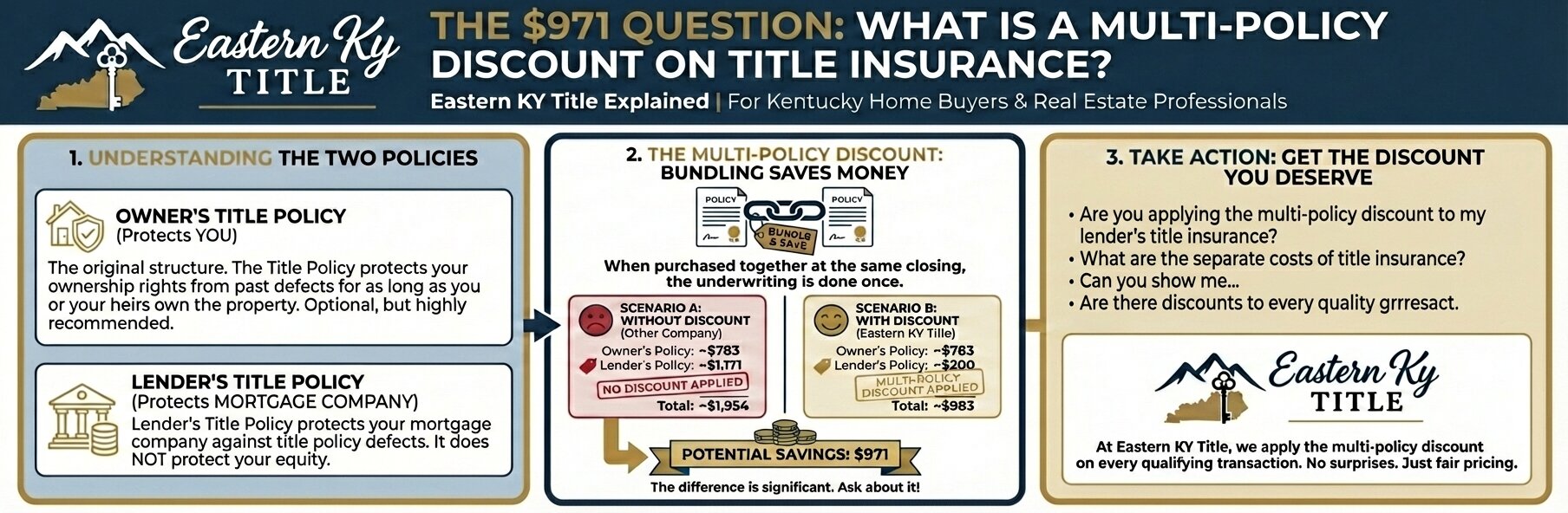

TL;DR: A multi-policy discount on title insurance means that when you buy an owner’s title policy AND a lender’s title policy together, the lender’s policy should be dramatically cheaper. At Eastern KY Title, that discount brings the lender’s policy down to around $200. We recently saw another title company skip this discount entirely and charge a buyer $1,171 for the same lender’s policy. That’s a $971 difference. Your title company choice matters more than you think.

You found the house. You negotiated the price. You got the inspection done. And now your closing disclosure lands in your inbox and somewhere in that wall of numbers is a line item called “lender’s title insurance” sitting at over a thousand dollars.

You don’t know whether that’s normal. Your agent doesn’t explain it. The title company doesn’t volunteer the information. So you sign where they tell you to sign and you pay what they tell you to pay.

That’s not a knock on you. That’s just how title insurance has worked in Kentucky for a long time. The companies that benefit from the confusion have very little incentive to clear it up.

I’m a real estate attorney. I’ve worked as a Kentucky Assistant Attorney General. I’ve been in more closings than I can count, and I’ve seen buyers get charged for things they didn’t have to pay for. The multi-policy discount is one of the most common ways buyers leave money on the table without even knowing there was money there to keep.

Let me fix that right now.

Title insurance comes in two varieties: owner’s title insurance, which protects you as the buyer, and lender’s title insurance, which protects your mortgage company. If you’re using a loan to purchase your home, your lender will almost certainly require you to buy that lender’s policy.

Here’s what most buyers never hear: when you purchase both policies at the same closing, the lender’s policy should be dramatically less expensive. That price reduction is called the multi-policy discount, and it’s built into how title insurance rates are structured.

Think of it exactly like bundling your home and auto insurance. You’ve done that before, right? You know that buying both through the same company gets you a better rate on each one. Title insurance works the same way. When a title company issues both the owner’s policy and the lender’s policy at the same time, the underwriting work is already done once. The search is complete. The risk has been assessed. Charging full price for the second policy on top of that is like your insurance agent charging you twice for the same inspection.

“The multi-policy discount isn’t a favor a title company does for you. It’s a discount that exists in the rate structure. The question is whether your title company passes it along.”

Lindon Gullett

I’ll tell you exactly what I saw last week, because this isn’t hypothetical.

A buyer was purchasing property in Eastern Kentucky. They obtained an owner’s title insurance policy for $783. That’s a reasonable number for a purchase of that size. But then the title company also charged that same buyer $1,171 for the lender’s title insurance policy.

Combined title insurance cost: $1,954.

At Eastern KY Title, here’s what that same transaction looks like. The owner’s policy would have been the same $783. The lender’s policy, with the multi-policy discount applied, would have been $200.

Combined title insurance cost: $983.

The difference is $971. Just under a thousand dollars, left on the table because the title company didn’t apply a discount that should have been standard.

| Scenario | Cost |

|---|---|

| Owner’s policy (both companies) | $783 |

| Lender’s policy (other company) | $1,171 — NO multi-policy discount applied |

| Lender’s policy (Eastern KY Title) | $200 — multi-policy discount applied |

| Buyer’s savings with Eastern KY Title | $971 SAVED |

Now, I want to be fair. Not every title company does this intentionally. Some of them are just running volume. They plug numbers into a system, generate a disclosure, and move on to the next file. They may not even realize their software isn’t applying the discount. That doesn’t make it right, but it explains why it happens.

Other companies make a very conscious choice. The discount is there. They just don’t use it.

Either way, the buyer pays the difference.

Here’s the blunt answer: because they can. There’s no law in Kentucky that forces a title company to automatically apply a multi-policy discount. It’s available in the rate structure, but applying it is a choice.

Corporate title companies doing hundreds of closings a month have less incentive to make sure every buyer gets every available discount. Their revenue model depends on volume and margin. If the buyer doesn’t know to ask, there’s no pressure to volunteer the savings.

We’re a different kind of operation. We’re not running a factory. We close deals across all 120 Kentucky counties, and we do it with a level of attention that a high-volume corporate shop simply cannot match. When John and I sit down on a file, we’re not trying to push it through as fast as possible. We’re looking at every number.

“Every line item on a closing disclosure is a decision. Either someone decided to charge it or decided not to. Buyers deserve to know which discounts exist and whether they’re getting them.”

That’s the standard we hold ourselves to on every file.

This is actually pretty simple. Before you sign anything, you have every right to ask your title company this direct question: “Are you applying the multi-policy discount to my lender’s title policy?”

If they hesitate, ask again. If they can’t explain it, that tells you something. A title company that understands its own rate structure can answer that question clearly in about thirty seconds.

You can also look at your closing disclosure. If you’re purchasing both an owner’s policy and a lender’s policy, and those two numbers are relatively close to each other, something may be off. The lender’s policy with a proper multi-policy discount should be significantly lower than the owner’s policy. In most Kentucky transactions we see, the lender’s policy comes out around $200 when the discount is applied correctly.

“Asking these questions isn’t rude. It’s your money. A good title company will answer every one of them without blinking.”

It matters more than people realize. Eastern Kentucky has a set of property issues that most corporate title companies treat as problems they’d rather not deal with. Severed mineral rights. Coal rights separated from surface rights decades ago. Heir property passed down through generations without formal documentation. Boundary disputes that trace back to old survey lines that nobody’s looked at since the 1970s.

These challenges show up in Breathitt County, in Pike, in Floyd, in Letcher, in Knott and Leslie and all the counties between. A title company that doesn’t know this region is going to flag these situations as uninsurable and send you home without a closing.

We handle them differently, because we know them. Lindon spent years as an Assistant Attorney General and has worked through more complicated Eastern Kentucky title situations than most title examiners see in an entire career. These properties aren’t problems to avoid. They’re problems we know how to fix.

The multi-policy discount matters in Lexington and Louisville too. But out here, in the counties where the property is complex and the closings are harder, your choice of title company carries even more weight. You need someone who can actually close your deal, at a fair price, and come to you if needed.

That’s what we do. Kitchen tables, front porches, hospital waiting rooms. We go where the client is.

Since we’re in the weeds on title insurance, let’s clear up a question that confuses a lot of buyers.

The lender’s title insurance policy protects the bank or mortgage company if something goes wrong with the title after closing. If a claim surfaces, the lender is protected. But here’s the catch: that policy protects the lender, not you. If you pay cash for a home, there’s no lender, so no lender’s policy is required. But you’re also unprotected.

The owner’s title insurance policy protects you. If someone files a claim against your title, if an old lien surfaces, if an heir comes forward claiming ownership, if there was a forgery somewhere in the chain of title, your owner’s policy covers you. It’s a one-time premium that protects you for as long as you own the property and even after you sell it, for claims that arose before your purchase.

Both policies are typically paid at closing, one time, and that’s it. No annual renewal, no monthly payments. That’s one of the most underappreciated things about title insurance. For the price of a few hundred to a few thousand dollars, you’re covered indefinitely.

Always, if you ask me. And I say that as someone who’s seen what happens when buyers skip it.

Paying cash? Get an owner’s policy. It’s not a lender’s requirement, so nobody’s forcing you. But title defects don’t care whether you paid cash or financed. If an old judgment lien surfaces or a boundary error comes to light, you’ll want that coverage.

Refinancing? In that case, a new lender’s policy is typically required but your existing owner’s policy remains in force. You don’t need to buy another owner’s policy. Ask your title company to confirm this clearly.

The process is straightforward, and we want you to understand it before we ever sit down together.

You’ll know your numbers before closing day. You won’t be surprised by a $1,171 lender’s policy charge when the discount should have brought it to $200. That conversation happens at the beginning, not after you’ve already committed.

Quick Answers to Your Top real estate Questions

Find answers to the most common questions about Eastern Kentucky real estate. If you can’t find the answer here, please contact us.

Our service offers a comprehensive set of features designed to help you manage your tasks. Key features include Feature A, FeatureKentucky title insurance rates are based on the purchase price or loan amount of the property. Owner’s policies and lender’s policies are priced according to established rate schedules. At Eastern KY Title, a lender’s title policy with the multi-policy discount applied typically runs around $200 when an owner’s policy is also being issued. For a precise quote on your transaction, contact us directly. B, and Feature C. You can find a full list and details on our Features Page.

In most cases, a title search in Eastern Kentucky takes between three and seven business days, depending on the county and how far back the chain of title needs to be traced. Some Eastern Kentucky counties have courthouse records that were damaged or destroyed in historical fires, which can require additional research. We work with experienced abstractors and build realistic timelines into every transaction.

No lender will require it since there’s no lender involved. But yes, we recommend it strongly. If a title defect surfaces after you purchase, an owner’s policy is the only coverage that protects you. Paying cash doesn’t eliminate the risk of past title problems. It just eliminates the requirement.

The multi-policy discount is a pricing reduction applied to the lender’s title insurance policy when it is issued at the same time and by the same company as an owner’s title insurance policy. It is built into standard title insurance rate structures. It is not legally required to be applied, but at Eastern KY Title, we apply it on every qualifying transaction.

Yes. In some real estate contracts, the seller selects and pays for the title search, but in many Kentucky transactions the buyer has input on which title company handles their closing. You are not obligated to use whoever your real estate agent or lender suggests, and it’s worth asking about pricing and the multi-policy discount before committing.

Yep. We are licensed to operate throughout Kentucky and regularly close deals across all 120 counties. We come to you, wherever you are. If you’re in Pike County or Johnson County or Breathitt County and need a mobile closing, that’s exactly what we do.

Lindon Gullett, Attorney at Law (Licensed in Kentucky) is President and Real Estate Attorney at Eastern KY Title. His career includes service as a Kentucky Assistant Attorney General, Staff Attorney with the Department of Public Advocacy, and years of hands-on legal practice across civil, criminal, and administrative matters. Lindon’s government and courtroom experience gives him exceptional skill at analyzing legal documents, clearing title defects, and protecting clients throughout transactions. Clients value his professionalism, reliability, and commitment to delivering smooth, secure closings.

Professional Licensure and Credentials:

If you’re purchasing property in Eastern Kentucky and you want to know exactly what your title insurance will cost before you ever get to the closing table, we’re easy to reach. We’ll walk you through the numbers, answer your questions, and tell you upfront whether the multi-policy discount applies to your transaction. No surprises. No $971 hidden charges. Just a clear, honest closing.

Contact Eastern KY Title today. Your kitchen table. Our office.

FULL DISCLOSURE: We use AI to draft our blog content because, frankly, we’d rather spend our time closing deals and helping Kentucky realtors than staring at blank screens. But don’t worry, we’re not letting the robots run wild. John and Lindon edit every single post to make sure it’s factually accurate, Kentucky-specific, and doesn’t sound like it was written by someone who thinks Appalachia is a type of pasta. If the AI writes something dumb, we fix it. If you spot something we missed, call us out. We’re good for it.