Address

234 Lower Gilmore Rd

Campton KY 41301

Work Hours

Monday to Friday: 9AM - 5PM

Address

234 Lower Gilmore Rd

Campton KY 41301

Work Hours

Monday to Friday: 9AM - 5PM

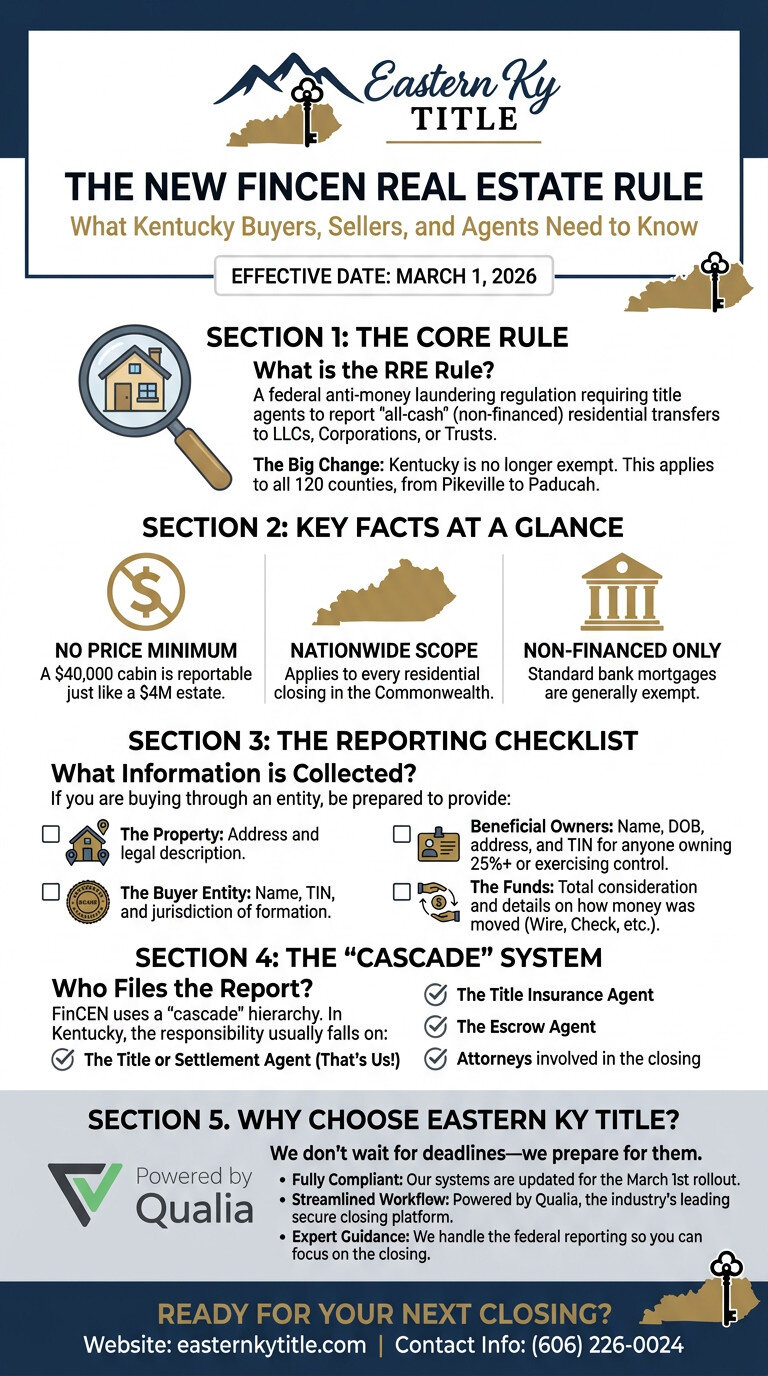

TL;DR: Starting March 1, 2026, the new FinCEN Residential Real Estate Rule requires title and settlement professionals to report certain all-cash transfers of residential property to LLCs, corporations, and trusts directly to the federal government. There is no minimum purchase price. The rule applies across all 50 states, including every county in Kentucky. At Eastern KY Title, we’re already compliant and ready to walk you through it.

Picture this: A buyer in Lawrence County makes an all-cash purchase of a home through their LLC. The deal closes clean, the deed gets recorded, and everybody shakes hands. Under the old system, that transaction slipped right past federal reporting requirements because Kentucky wasn’t covered by FinCEN’s Geographic Targeting Orders.

Starting March 1, 2026, that changes.

The Financial Crimes Enforcement Network, better known as FinCEN, has finalized a rule that sweeps away the old patchwork system of city-by-city targeting orders and replaces it with a permanent, nationwide reporting requirement. If you’re a buyer taking title through a legal entity or trust, or a real estate professional involved in those closings, this rule is going to affect how your deals get done.

The good news? At Eastern KY Title, we’ve been preparing for this for months. We’re powered by Qualia, one of the most advanced closing platforms in the country, which means we already have the infrastructure in place to collect, track, and report the required information accurately and on time. You won’t be scrambling at the closing table. We already sorted that out so you don’t have to.

FinCEN’s new Residential Real Estate Rule is a federal anti-money laundering regulation that took its final form under the Bank Secrecy Act. The rule requires designated “reporting persons,” which in most transactions means the title or settlement agent, to file a Real Estate Report (RER) with FinCEN whenever a non-financed transfer of residential real property is made to a legal entity or trust.

In plain English: if someone buys a house with cash (or private financing, seller financing, or anything other than a traditional bank mortgage) and takes title in the name of an LLC, corporation, partnership, or trust, that transaction must now be reported to the federal government.

Key facts at a glance:

This is where it gets interesting, and honestly, where a lot of deals could get tangled up if the professionals involved aren’t paying attention.

To ensure compliance with the FinCEN Residential Real Estate Rule, FinCEN created what they call a “cascade” system to assign reporting responsibility. There’s a hierarchy of seven different functions, and responsibility falls to the first person in that hierarchy who is actually involved in the closing. The list generally starts with:

In Kentucky, because we’re a title attorney state and most closings involve legal counsel, the reporting responsibility will often land with the closing attorney or title agent. That’s us. And that’s exactly why we got ahead of this.

Professionals can also enter into written designation agreements to shift reporting responsibility between eligible participants. As John Holder, our Market President, puts it: “The cascade system sounds complicated until you map it out step by step. Once you understand which function applies to your role in a given transaction, the path to compliance is actually pretty clear.”

The cascade system sounds complicated until you map it out step by step. Once you understand which function applies to your role in a given transaction, the path to compliance is actually pretty clear.

The Real Estate Report that gets filed through FinCEN’s BSA E-Filing System requires a significant amount of identifying information. Here’s what the rule calls for:

That last item, the beneficial ownership information, is the teeth of this rule. The whole point is to pierce the veil of anonymous LLCs and trusts that have historically been used to launder money through real estate.

For our clients in Eastern Kentucky, this mostly means additional paperwork upfront. If you’re buying through an LLC or trust, be prepared to share documentation about who actually owns and controls that entity. Not a burden if you’re a legitimate buyer. Exactly the right question if you’re not.

Yes, it does. Under the FinCEN Residential Real Estate Rule, covered properties include:

Here’s a nuance worth noting: a property can be mixed-use and still be covered. A home sitting above a small commercial space, which isn’t uncommon in smaller Eastern Kentucky towns, can still qualify as reportable residential real property.

What’s NOT covered: transfers directly to individuals (not entities or trusts), and transfers involving traditional bank financing subject to federal anti-money laundering requirements.

The limited exemptions include transfers due to death, divorce, certain bankruptcy proceedings, and some Section 1031 exchange transactions. These exemptions are narrowly written and need to be evaluated carefully on a case-by-case basis.

Here’s something worth thinking about. The old Geographic Targeting Orders were focused on high-value markets in places like Miami, Manhattan, and parts of California. Kentucky was largely outside their reach.

That changes completely on March 1, 2026.

Eastern Kentucky has a unique real estate market. There are properties that have passed through multiple generations of heirs without clear title. We have land with severed mineral and coal rights. Farms, hollows, and ridge-top tracts get transferred between family LLCs as part of estate planning strategies. Many of these transactions happen without traditional bank financing.

A family in Floyd County that transfers land to a family LLC for estate planning purposes may now trigger a federal reporting requirement, even if the transfer involves no cash at all. Gift transfers are covered. Zero-dollar deeds to entities are covered.

This doesn’t mean anything nefarious is assumed. FinCEN is clear that there are plenty of legitimate reasons to hold property in an entity or trust. The rule is about transparency, not accusation. But it does mean the paperwork just got more involved, and the people at your closing table need to know what they’re doing.

We made the decision early on to build our operation around Qualia, the closing platform that leading title companies across the country rely on for compliance, workflow management, and reporting accuracy. That wasn’t a coincidence. It was a deliberate choice to make sure that when federal mandates like the FinCEN Residential Real Estate Rule take effect, we weren’t scrambling.

As John puts it: “Compliance isn’t something you bolt on at the last minute. It’s something you build into your process from day one. Qualia gives us the framework to make sure nothing falls through the cracks, from the initial title search through the final filing.”

Compliance isn’t something you bolt on at the last minute. It’s something you build into your process from day one. Qualia gives us the framework to make sure nothing falls through the cracks, from the initial title search through the final filing.

John Holder | Eastern KY Title

That infrastructure matters for our clients because it means your closing isn’t going to be delayed by paperwork surprises. We know what to ask, we know when to ask it, and we know how to file accurately and on time.

Reports must be filed by the later of 30 calendar days after closing or the last day of the month following the month of closing. That’s a tight window when you’re also managing the post-close to-do list. Qualia keeps us on track.

If you’re buying residential property through an LLC, corporation, partnership, or trust without traditional bank financing, here’s what to have ready before closing:

The earlier you get this to us, the smoother things go. We’re not going to spring this on you at the closing table.

If you have questions about how FinCEN’s new Residential Real Estate Rule affects your closing in Kentucky, you’re not alone. Below are the most common questions we’re fielding from buyers, sellers, investors, and real estate agents, along with straight answers based on the rule as written and our experience on the ground.

No. If your purchase is financed by a traditional lender subject to federal anti-money laundering requirements, the transaction is generally excluded from the rule. The rule targets non-financed, all-cash, private, or seller-financed transfers to legal entities and trusts.

The rule doesn’t distinguish between business LLCs and family holding entities. If the transferee is a legal entity or trust and the transfer is non-financed, it’s potentially reportable. The good news is that reporting doesn’t imply wrongdoing. It just means we file the paperwork.

Absolutely yes, and arguably even more so. When you pay cash, there’s no lender requiring a title search as a condition of the loan. That protection falls entirely on you. Owner’s title insurance through Stewart Title protects your investment against title defects, prior liens, and claims you didn’t know about at the time of purchase. Without a mortgage, nobody’s looking out for you but your title company.

Title insurance in Kentucky is regulated by the Kentucky Department of Insurance and rates are based on the purchase price or loan amount. For a general ballpark, most owner’s policies on a $150,000 home run in the range of $600 to $900 for a one-time premium that lasts as long as you own the property. Contact us for a specific quote.

It depends on the property. A straightforward residential property with a clean, modern chain of title can be searched in two to three business days. Properties in Eastern Kentucky with complex histories, including severed mineral rights, heir property situations, or courthouse record gaps from historical courthouse fires, can take longer. We’ll tell you upfront what we’re dealing with and keep you informed throughout.

In most Kentucky closings, that responsibility will fall to the title or settlement agent under the cascade system, which means it falls to us. We file the report. You provide the required information about the entity or trust taking title. We handle the rest.

FinCEN has civil and criminal penalty authority under the Bank Secrecy Act for willful non-compliance. Penalties can be substantial. This is not optional paperwork.

Yes and no. The new RRE Rule creates a permanent nationwide reporting regime that will replace the current residential real estate GTO framework once it takes effect. Until then, FinCEN’s existing real estate GTOs remain in force through their stated expiration date and continue to govern covered transactions in the designated areas.

Lindon Gullett, Attorney at Law (Licensed in Kentucky) is President and Real Estate Attorney at Eastern KY Title. His career includes service as a Kentucky Assistant Attorney General, Staff Attorney with the Department of Public Advocacy, and years of hands-on legal practice across civil, criminal, and administrative matters. Lindon’s government and courtroom experience gives him exceptional skill at analyzing legal documents, clearing title defects, and protecting clients throughout transactions. Clients value his professionalism, reliability, and commitment to delivering smooth, secure closings.

Professional Licensure and Credentials:

FULL DISCLOSURE: We use AI to draft our blog content because, frankly, we’d rather spend our time closing deals and helping Kentucky realtors than staring at blank screens. But don’t worry, we’re not letting the robots run wild. John and Lindon edit every single post to make sure it’s factually accurate, Kentucky-specific, and doesn’t sound like it was written by someone who thinks Appalachia is a type of pasta. If the AI writes something dumb, we fix it. If you spot something we missed, call us out. We’re good for it.