Address

234 Lower Gilmore Rd

Campton KY 41301

Work Hours

Monday to Friday: 9AM - 5PM

Address

234 Lower Gilmore Rd

Campton KY 41301

Work Hours

Monday to Friday: 9AM - 5PM

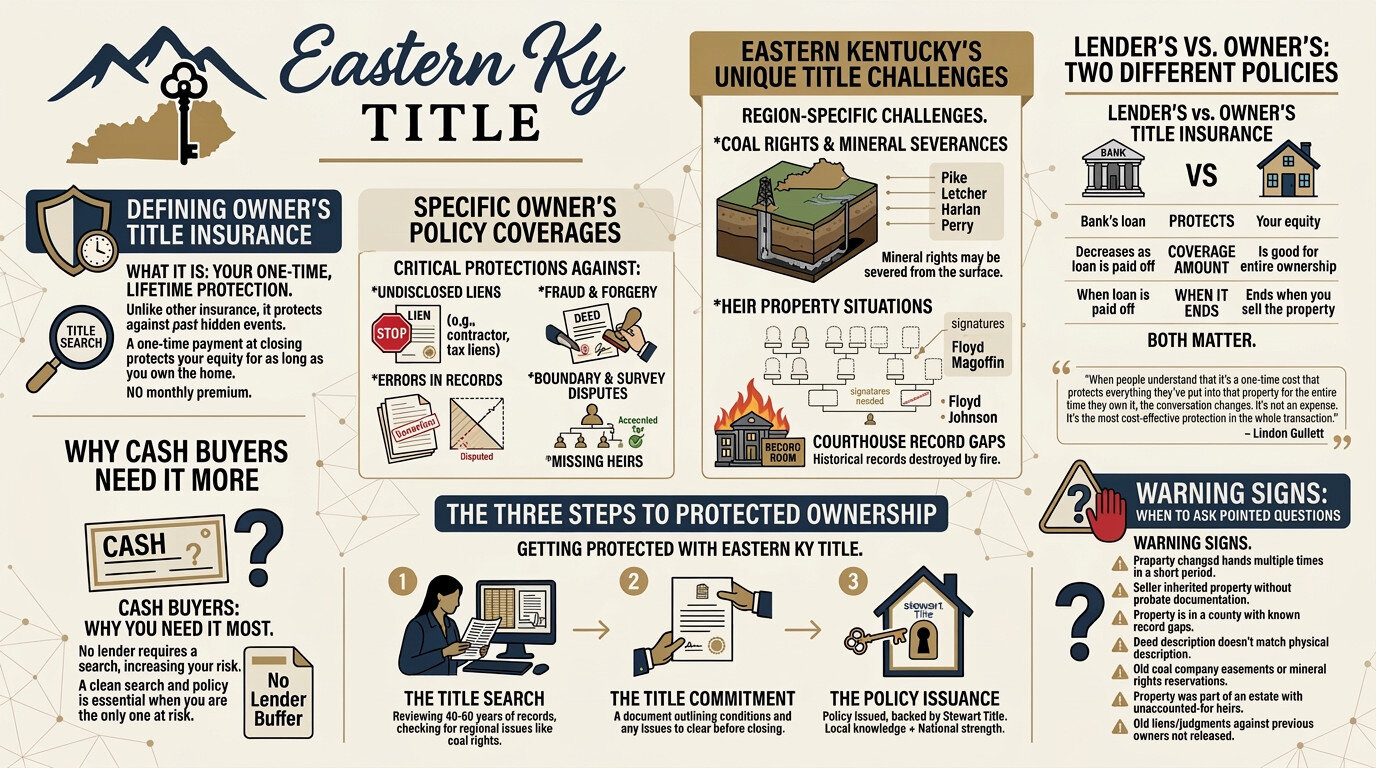

TL;DR: Owner’s title insurance is a one-time purchase that protects your property rights for as long as you own your home. It covers hidden title defects, ownership disputes, and legal costs that could surface years after closing. In Eastern Kentucky, where coal rights severances, heir property situations, and courthouse record gaps are common, it’s not just smart — it’s essential.

You’ve found the house. You’ve survived the inspection. You’ve made it through the loan process — which, if you’ve done it recently, felt about as relaxing as defusing a bomb while someone explains the forms to you.

And then somebody hands you a stack of papers at closing and says, “This one’s for title insurance.” You sign it. You don’t think about it again.

Until the day you do.

Maybe it’s a neighbor who shows up claiming they own part of your yard. Maybe it’s a collection agency for a contractor who supposedly did work on the property two owners ago. Maybe it’s a long-lost heir who just realized their grandmother owned your house and nobody told them it was sold.

These aren’t hypotheticals. They happen. And in Eastern Kentucky, where property history can stretch back through generations with records scattered across courthouse fires, coal company transfers, and handshake deals, they happen more than people realize.

That’s exactly why owner’s title insurance exists. And it’s exactly why understanding it before you need it matters.

Owner’s title insurance is a policy that protects your legal right to own and use your property. Unlike homeowner’s insurance, which protects against future events like fires or floods, title insurance protects against past events — problems that existed before you ever signed the deed but might surface after closing.

Here’s the key: you pay for it once, at closing, and it’s good for the entire time you own the property. There’s no monthly premium. No renewal. It just sits there, quietly doing its job, until you need it.

The policy is issued based on a title search — a review of public records to verify the chain of ownership and identify any existing claims or defects. But even a thorough title search can’t catch everything. That’s the gap owner’s title insurance fills.

This is where people get fuzzy. So let’s be specific.

If someone comes forward with a legitimate claim that they have an ownership interest in your property — a missing heir, a forged deed, an improperly recorded transfer — your policy covers your legal defense and any financial loss up to the policy amount.

Courthouse records aren’t perfect. A clerical error in a deed, a misfiled document, an incorrect legal description — these can cloud title years after a transaction closed. Owner’s title insurance covers losses resulting from these kinds of errors.

A previous owner didn’t pay their contractor. Or their property taxes from three years ago went delinquent and nobody caught it. Or there’s a mechanic’s lien from work done before the sale. If those liens weren’t discovered at closing and they attach to your property, title insurance has your back.

Your fence is where it’s always been. Your neighbor disagrees. If a boundary dispute escalates into a legal claim against your title, a good owner’s policy covers the cost of defending your position.

This one’s more common than you’d think. If a previous transfer in the chain of title involved a forged signature or fraudulent transaction, and that fraud affects your ownership rights, title insurance covers the resulting loss.

This is especially relevant in Eastern Kentucky. Properties that have passed through families for generations sometimes skip proper probate. An heir who should have received notice didn’t. That heir can, legally, come back and make a claim. Owner’s title insurance covers you when they do.

I’ve been handling real estate transactions in this region for over 30 years. I’ve worked as a Master Commissioner in Lewis County. I’ve written a book on Kentucky notary law. And I’ll tell you straight: Eastern Kentucky title work is not the same as title work in Louisville or Lexington.

Here’s what makes it different.

Decades of coal industry activity left a complicated paper trail across Appalachian Kentucky. In counties like Pike, Letcher, Harlan, and Perry, mineral rights were routinely severed from surface rights, sometimes long before anyone alive today was born. If you’re buying property and nobody checks the mineral rights history, you could end up owning the surface while someone else owns what’s underneath it. Owner’s title insurance, combined with a thorough title search, is your protection here.

A family owns land for generations. The original owner dies without a will. The land passes informally to children, then grandchildren, some of whom may have moved out of state. Nobody recorded the transfers. When one family member wants to sell, suddenly you need to track down and get signatures from a dozen people — some of whom may not even know they have an ownership interest.

We’ve helped buyers and sellers navigate exactly these situations across Floyd, Johnson, and Magoffin counties. They’re solvable. But they take local knowledge, persistence, and a title company that doesn’t run from complicated.

Several Eastern Kentucky courthouses suffered fires over the decades, destroying historical records. When the chain of title has gaps, a thorough search requires more than just pulling digital records. It requires knowledge of where the gaps are, what substitute records exist, and how to document a clean chain of ownership even when the standard paper trail has holes in it.

If you’re financing your home purchase, your lender will require title insurance. But here’s what catches buyers off guard every time: that policy protects the lender, not you.

Lender’s title insurance covers the bank’s financial interest in the property up to the loan amount. As you pay down your mortgage, the coverage decreases. When the loan is paid off, the coverage ends.

Owner’s title insurance is separate. You purchase it at closing, typically for a one-time premium based on the purchase price, and it protects your equity and ownership rights for the life of your ownership. If you sell the property in 20 years and a title defect surfaces during that transaction, your original policy may still provide protection.

Two policies. Two different sets of protection. Both matter.

The one-time premium is based on the purchase price of the property and is regulated by the state of Kentucky. For most home purchases in Eastern Kentucky, you’re looking at a few hundred dollars, though the exact amount depends on the purchase price and the specific coverage.

Here’s the math that matters: you pay once, and the coverage lasts as long as you own the property. Compare that to the potential cost of a title dispute — which can easily run into tens of thousands of dollars in legal fees, lost equity, or both — and the premium is a straightforward decision.

As Lindon puts it, “When people understand that it’s a one-time cost that protects everything they’ve put into that property for the entire time they own it, the conversation changes. It’s not an expense. It’s the most cost-effective protection in the whole transaction.”

When people understand that it’s a one-time cost that protects everything they’ve put into that property for the entire time they own it, the conversation changes. It’s not an expense. It’s the most cost-effective protection in the whole transaction.

Lindon Gullett

Yes. In fact, if you’re paying cash, you need it more.

When you finance a property, the lender requires a title search and lender’s title insurance as part of the process. That means at minimum, a professional is reviewing public records and flagging problems. Cash buyers sometimes skip that process entirely, which is how people end up with title problems they don’t discover until they try to sell.

A clean title search and owner’s title insurance policy is just as important when you’re the only one at risk. More so, actually, since there’s no lender standing between you and potential liability.

Here’s how the process works when you work with Eastern KY Title:

We review public records for the property, typically going back 30 to 60 years depending on the situation. We’re looking at deeds, liens, judgments, tax records, easements, and anything else that could affect the chain of title. In Eastern Kentucky, we also check for coal rights severances, mineral reservations, and other region-specific issues that a national title company might not know to look for.

Based on the search, we issue a title commitment — a document that outlines the conditions under which we’ll insure the title. Any issues found during the search are listed as exceptions or requirements. Requirements are problems that need to be cleared before closing. Exceptions are items that will be excluded from coverage.

After closing, once all requirements have been satisfied, we issue the owner’s title insurance policy. The policy is backed by Stewart Title, one of the largest and most respected title insurance underwriters in the country. That combination — our local knowledge and hands-on service, backed by Stewart Title’s financial strength — is what makes Eastern KY Title different.

Not every title situation is complicated. But here are scenarios where you should be asking your title company some pointed questions:

These aren’t deal-killers. Most of them are solvable. But they require a title company that’s done this work before and isn’t going to panic at the first sign of complexity.

Premiums are set by state regulation and based on the purchase price. For most residential transactions in Eastern Kentucky, expect a one-time premium in the range of a few hundred dollars. Your closing disclosure will show the exact amount. The important thing to remember: you pay it once, and it’s good for the entire time you own the property.

For a straightforward residential transaction, typically 2-5 business days. Properties with complicated histories, gaps in the chain of title, or mineral rights issues may take longer. We’ll tell you upfront what we’re dealing with and give you a realistic timeline.

Absolutely. Without a lender requiring a search, cash buyers have no external check on the title. If anything, cash buyers need to be more diligent about title insurance, not less.

Lender’s insurance protects the bank. Owner’s insurance protects you. You need both when financing. If you’re paying cash, there’s no lender policy — just the owner’s policy, which is even more important.

Yes, and they do. Missing heirs, previously undisclosed liens, fraud in the chain of title — these can surface years or even decades after a purchase. Owner’s title insurance covers you regardless of when the problem surfaces, as long as it stems from something that occurred before your closing date.

It depends on the nature of the defect. Some issues — like an old lien that can be paid off or a corrective deed that clears a recording error — can be resolved before closing. Others may require more work. We’ll walk you through exactly what we found, what it means, and what the options are.

Coverage depends on your specific policy and the nature of the dispute. Many standard owner’s policies cover boundary disputes that affect your title. An enhanced policy typically provides broader coverage. Ask about the specific policy terms when you’re reviewing your commitment.

This is common in our region. The title search will identify whether mineral rights have been severed. Your policy will include that as an exception — meaning you’ll know upfront that mineral rights are not part of what you’re purchasing. That’s different from a surprise discovery after closing. Knowledge is protection.

John Holder, Attorney at Law (Licensed in Kentucky) is Market President and Title Agent at Eastern KY Title. With over 30 years of legal experience and thousands of closings completed as a loan signing agent, John leads operations with a legal-first approach built on experience in real estate law, business development, and risk mitigation. He’s known for simplifying complex transactions and his commitment to digital security and client education. John is also the founder of Kentucky Notaries and author of “Kentucky Notary Law & Practice: A Modern Guide.”

Professional Licensure & Credentials:

Whether you’re buying your first home in Johnson County, handling a complicated estate property in Pike County, or navigating a transaction with decades-old legal description issues in Greenup County — we’re ready to help.

Eastern KY Title brings your closing to you. Your kitchen table. Your timeline. Our job.

Call us today to talk through your transaction. No corporate hold music. No out-of-state call center. Just local expertise, backed by Stewart Title, delivered the way business used to be done in Eastern Kentucky.

Contact Eastern KY Title: (606) 226-0024

Best regards, Eastern KY Title Team

FULL DISCLOSURE: We use AI to draft our blog content because, frankly, we’d rather spend our time closing deals and helping Kentucky realtors than staring at blank screens. But don’t worry, we’re not letting the robots run wild. John and Lindon edit every single post to make sure it’s factually accurate, Kentucky-specific, and doesn’t sound like it was written by someone who thinks Appalachia is a type of pasta. If the AI writes something dumb, we fix it. If you spot something we missed, call us out. We’re good for it.