Address

234 Lower Gilmore Rd

Campton KY 41301

Work Hours

Monday to Friday: 9AM - 5PM

Address

234 Lower Gilmore Rd

Campton KY 41301

Work Hours

Monday to Friday: 9AM - 5PM

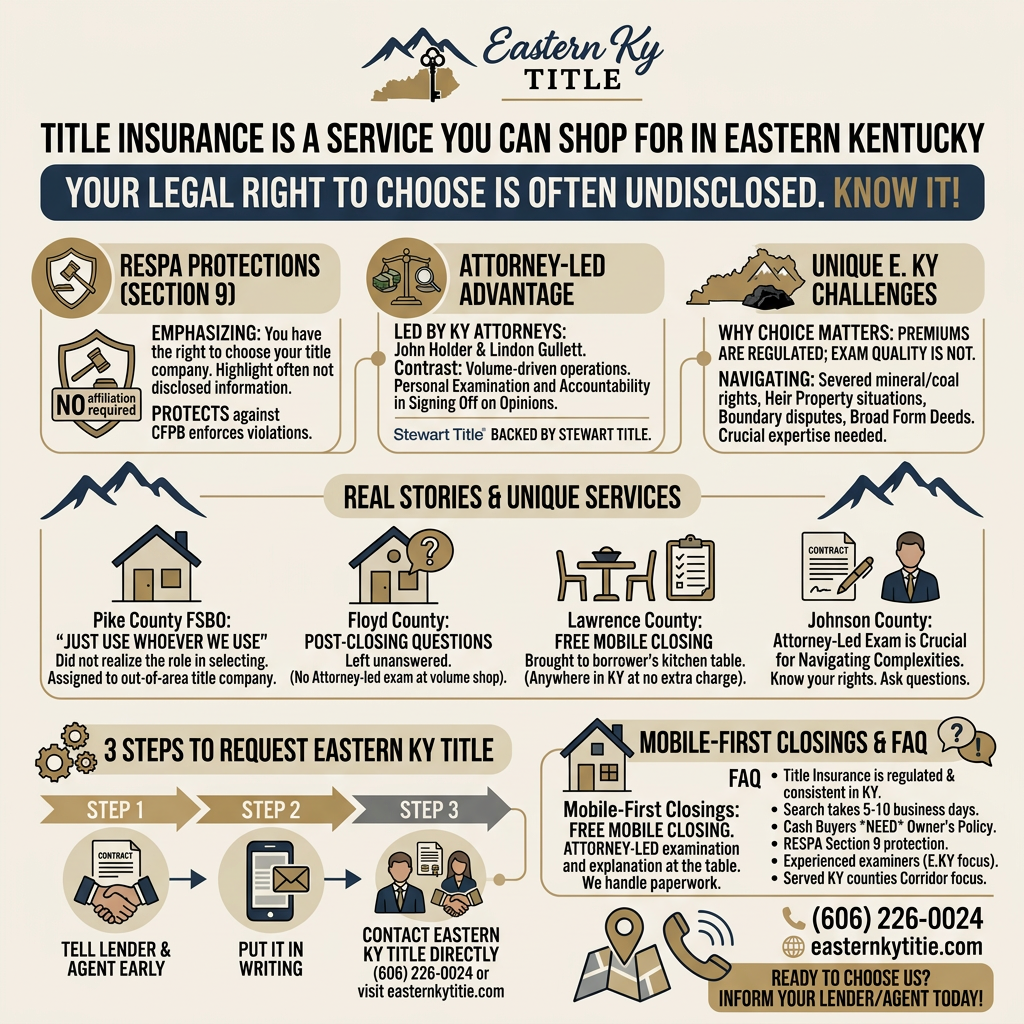

TL;DR: In most financed home purchases, federal law (RESPA Section 9) prohibits the seller from requiring you to use a particular title company as a condition of the sale. Nobody is required to tell you that. Here is what that right means, why it matters in Eastern Kentucky, and how to use it.

We get a version of this call about once a month. Someone bought a house, used whoever the lender or agent pointed them to, and now they have a question. Maybe it is about a coal rights reservation buried in the deed chain. Maybe a neighbor is disputing a boundary. Maybe they found out after closing that there was an heir whose name was missed.

The title company they used? They have a call center. Nobody who actually worked their file still works there. And the person on the phone has never heard of Letcher County.

We are not telling that story to make anyone feel bad. We are telling it because the person on the other end of that call always says the same thing: “I didn’t know I could choose.”

You can. You always could. Here is everything you need to know.

The Real Estate Settlement Procedures Act, specifically Section 9, makes it illegal for a seller to require you to use a particular title company as a condition of sale. RESPA also restricts undisclosed kickbacks and affiliated business arrangements that can quietly inflate your costs, and requires clear disclosures when there is an ownership or referral relationship between your lender, agent, and title company.

The Consumer Financial Protection Bureau enforces RESPA violations. The law exists because, without it, kickbacks and affiliated business arrangements could quietly inflate your closing costs and reduce the quality of your title examination.

In plain terms: the title company is your choice. Not the seller’s. Not the lender’s. Not the agent’s.

In some transactions, the seller can “require” a particular provider only if the seller pays 100% of title insurance and related title costs, which is treated as an exception to Section 9.

Here is a question worth sitting with. When you buy a home in Floyd County or Johnson County or anywhere else in Eastern Kentucky, who is actually reading the title abstract? Who is deciding whether that 1962 coal severance deed is a problem? Who is signing off on the opinion that makes your lender and your insurance carrier comfortable?

That decision shapes whether your closing goes smoothly and whether you have real protection if something surfaces later. Title insurance is not like shopping for a phone plan. The premium is roughly the same wherever you go in Kentucky. The quality of the examination behind it is not.

As Lindon Gullett, our founder and a former Kentucky Assistant Attorney General, puts it: “Title insurance premium rates are filed and regulated in Kentucky, so your cost is usually similar no matter which company you use. The real difference is the quality of the title examination and the attorney behind it.”

Title insurance premium rates are filed and regulated in Kentucky, so your cost is usually similar no matter which company you use. The real difference is the quality of the title examination and the attorney behind it.

Not every title company is run by attorneys. Not every closing is conducted by someone who has read the file.

At Eastern KY Title, both principals are licensed Kentucky attorneys. John Holder and Lindon Gullett personally examine the title abstracts prepared by Stewart Title and issue the opinions themselves. When a complex issue surfaces, the person reviewing it has the same legal training as the person who would represent you in court.

That is not the standard at volume-driven title operations where closings are processed by the dozen and shipped off to a central underwriting hub somewhere out of state.

As John puts it: “We sign our name to every opinion. That accountability tends to focus the mind.”

There is a version of title work that is essentially clerical. The property last sold five years ago, the chain is clean, and the closing is routine. That version exists everywhere.

Then there is Eastern Kentucky.

The title challenges that come through our door on a regular basis include:

Broad form deeds executed in the early 20th century routinely severed surface rights from mineral rights across Appalachian Kentucky. Decades later, those severances are still active, still recorded, and still catch buyers off guard.

Rural Eastern Kentucky has generations of property that passed without formal probate. When a family wants to sell, the question of who actually holds title can require tracing heirs across multiple generations and sometimes multiple states.

Survey inconsistencies, missing plat references, and recorded deeds with ambiguous metes-and-bounds descriptions are common in counties where some land was never formally platted.

A title examiner unfamiliar with Eastern Kentucky legal history will not necessarily know what to look for. We do, because we have been doing this work here for decades.

A buyer in Pike County contacted us after their closing with questions about a mineral rights reservation their deed referenced. When they reached out to the title company they had used, they were transferred twice and never received a clear answer.

They had been told at the outset to “just use whoever we use.” Nobody told them they had a choice. When we reviewed the situation, the reservation was something that had been disclosed but not fully explained. An attorney-led examination and a pre-closing conversation could have addressed their questions before the ink was dry.

A borrower in Lawrence County was scheduled to drive 45 minutes to a bank branch for a refinance closing. They did not know that under Kentucky law and with the right title company, a mobile closing is an option. We brought the closing to them. They signed at their kitchen table. The whole thing took less than an hour.

A buyer in Floyd County used the lender’s default title company for their purchase. After closing, they had concerns about an access easement referenced in the title commitment. When they called the title company, they were told to consult an attorney.

The people who issued their title opinion were not attorneys. We are. That distinction exists before closing, not just after.

A seller in Johnson County listing their property without an agent assumed the lender would “handle” the title work. They did not realize they had any role in selecting a title company or that they had rights under RESPA. By the time they contacted us, the transaction had already been assigned to an out-of-area title company. We walked them through what had happened and what their options were.

In a FSBO (For Sale By Owner) transaction, the absence of a listing agent does not eliminate your right to choose. It just means nobody is there to tell you about it.

If you are a buyer, seller, or borrower in Eastern Kentucky, the process is straightforward:

That is the whole plan. Three steps. No confrontation required.

We are a mobile-first operation. We bring the closing to you, anywhere in Kentucky, at no additional charge. Attorney-led. Attorney-examined. Backed by Stewart Title’s underwriting. We handle the paperwork, explain everything at the table, and answer the phone when you have questions after closing.

We are not the biggest title company in Kentucky. We are not trying to be. We are trying to be the right title company for the deals that matter, in the counties we know, for the people who deserve an expert in their corner.

We get a lot of the same questions. That is not a complaint. It means people are doing their homework before they sign anything, which is exactly what we want. Here are the ones that come up most often.

Title insurance premiums in Kentucky are regulated by the state, which means the rate is largely consistent regardless of which company you choose. The cost is typically calculated as a percentage of the purchase price or loan amount. Owner’s policies and lender’s policies are separate and serve different purposes.

For straightforward transactions in well-maintained counties, a title search typically takes five to ten business days. In counties with complex histories, missing records, or mineral severances, it can take longer. We communicate timeline expectations upfront so there are no surprises.

Yes. A lender’s policy only protects the lender. If you are paying cash, there is no lender’s policy at all. Owner’s title insurance is the only protection you have against title defects that surface after closing. In Eastern Kentucky, where chain-of-title issues are genuinely common, skipping owner’s coverage is a meaningful risk.

A lender’s policy protects the bank. An owner’s policy protects you. They are not interchangeable. Most lenders require their own policy as a condition of the loan, but that coverage disappears when the loan is paid off and it never covered you to begin with. Owner’s coverage stays with you for as long as you own the property.

Yes. RESPA Section 9 makes it illegal for a seller to require you to use a specific title company as a condition of sale. You can always request a different title company.

Severed mineral rights, broad form deed legacy issues, heir property with missing probate records, and courthouse record gaps are significantly more common in Eastern Kentucky than in other regions. Experience with these issues matters. Not every title examiner has it.

A mobile closing means we come to you, wherever you are in Kentucky, rather than requiring you to drive to an office. We do not charge an additional fee for this. It is simply how we work.

Our team combines legal expertise, local knowledge, and a commitment to client protection. Led by Market President John Holder and President Lindon Gullett (both licensed Kentucky attorneys), we deliver secure, accurate, and stress-free real estate closings for families, lenders, and real estate professionals across Eastern Kentucky.

Our Team:

John Holder – Market President and Title Agent, Attorney at Law (Licensed in Kentucky)

Lindon Gullett – President and Real Estate Attorney, Attorney at Law (Licensed in Kentucky), Former Kentucky Assistant Attorney General

Professional Credentials:

Both principals are licensed attorneys, verified in the KBA Attorney Directory. Eastern KY Title is backed by Stewart Title Guaranty Company, one of the largest title underwriters in the country.

Best regards, Eastern KY Title Team

Call us at (606) 226-0024 or visit easternkytitle.com/contact to start the conversation. If you are already under contract, let your agent and lender know you are requesting Eastern KY Title. We will handle everything from there.

FULL DISCLOSURE: We use AI to draft our blog content because, frankly, we’d rather spend our time closing deals and helping Kentucky realtors than staring at blank screens. But don’t worry, we’re not letting the robots run wild. John and Lindon edit every single post to make sure it’s factually accurate, Kentucky-specific, and doesn’t sound like it was written by someone who thinks Appalachia is a type of pasta. If the AI writes something dumb, we fix it. If you spot something we missed, call us out. We’re good for it.